Posts with tag 'buying a home'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2024 | 5 Posts

- 2023 | 37 Posts

- 2022 | 43 Posts

- 2021 | 31 Posts

- 2020 | 29 Posts

- 2019 | 17 Posts

- 2018 | 22 Posts

- 2017 | 14 Posts

- 2016 | 23 Posts

- 2015 | 12 Posts

- 2014 | 2 Posts

9

Top 5 Reasons You Need a Real Estate Agent When Buying a House

If you are looking to buy or sell a home in the near future, here's something you need to know – expert advice from a trusted real estate agent is priceless, more now more than ever. And here's why.

A real estate agent does a lot more than you may realize.

Your agent is the person who will guide you through every step when buying a home and look out for your best interests along the way. They smooth out a complex process and take away the bulk of the stress of what's likely your largest purchase ever. And that's exactly what you want and deserve.

This is at least a part of the reason why a recent survey from Bright MLS found an overwhelming majority of people agree an agent is...

16

Have you decided to buy a new construction home? Having your own agent matters.

If you've been searching for your dream home for some time and have been challenged with low inventory, you're not alone.

Right now, the supply of homes for sale is still low. But there is a bright spot. Newly built homes make up a larger percentage of the total homes available for sale than normal. That's why, if you're craving more options, it makes sense to see if a newly built home is right for you.

But it's important to remember the process of working with a builder is different than buying from a homeowner. And, while builders typically have sales agents on-site, having your own agent helps make sure you have proper representation throughout your home-buying journey. As Realtor.com says:

6

Why Use a REALTOR®

A REALTOR® is an expert in their profession who will expertly guide you through the complicated process of a home purchase or sale. Your REALTOR®'s job is to ensure the process is done correctly, navigating the contracts and negotiations on your behalf and help you get the most out of one of the biggest investments in your life.

Other reasons to use a REALTOR® according to www.virginiarealtors.org:

Think all real estate agents are REALTORS®? Think again!

RE...

7

Becoming A Home Maintenance Pro: Tips For New Homeowners

Buying a house is a big achievement and also the start of a long, rewarding journey. As a new homeowner, you have a lot on your plate getting familiar with your new dwelling, moving all of your possessions, and getting used to making mortgage payments. Home improvement will also become an important part of life moving forward, and it's wise to start on home maintenance tasks as soon as possible once you move in. Start your life as a new homeowner on the right foot with our guide to becoming a home maintenance pro.

- Start with a Deep Cleaning

Ideally, the home should be spotless when you move in, but it doesn't hurt to make sure every corner has been scrubbed. In addition to all the usual home improvement benefits of cleaning, scouring every corner of the house will help you spot any maintenance issues. Be sure to clean the areas around appliances, chec...

6

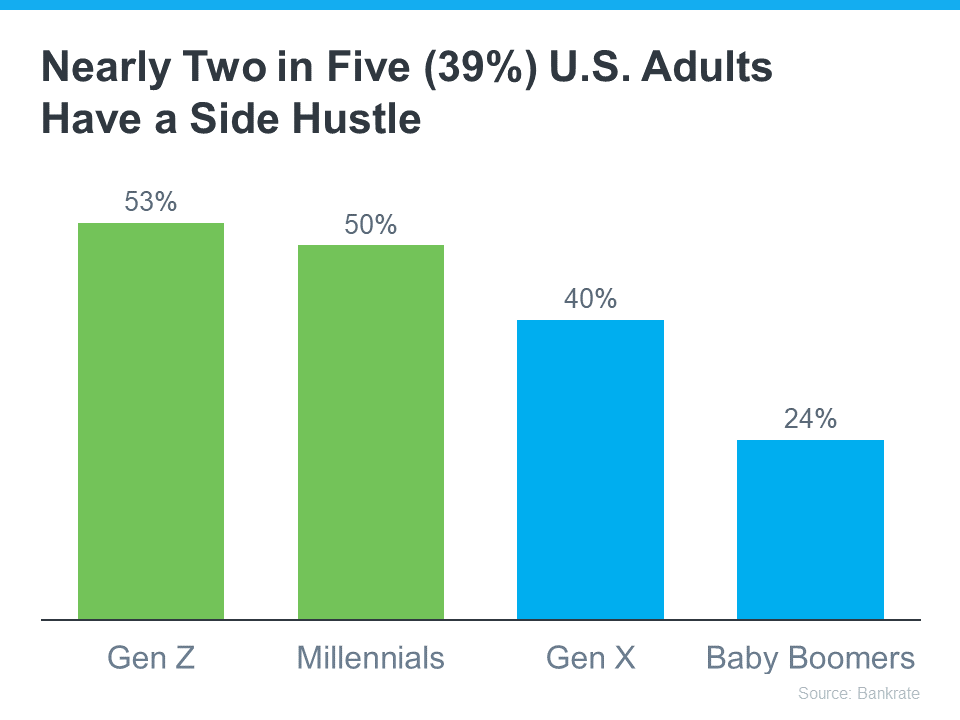

Creative Options for Your Homeownership Quest

It may be time to consider creative options in your quest to become a homeowner. Think of a new home as a side hustle and not just in earned equity.

Does the rising cost of just about everything these days make your dream of owning your own home feel less within reach?? According to Bankrate, many people are seeking additional income through side hustles, possibly to cope with those increasing expenses and save for a home. This trend is particularly popular with younger individuals who may be dealing with student loan debt (see graph below):