Posts in category 'Buying A Home'

Subscribe and receive email notifications of new blog posts.

RSS Feed

RSS Feed

- 2024 | 5 Posts

- 2023 | 37 Posts

- 2022 | 43 Posts

- 2021 | 31 Posts

- 2020 | 29 Posts

- 2019 | 17 Posts

- 2018 | 22 Posts

- 2017 | 14 Posts

- 2016 | 23 Posts

- 2015 | 12 Posts

- 2014 | 2 Posts

21

Celebrate Earth Day Everyday... Plant a Pollinator Garden.

It doesn't take much effort to Give back to our Earth. This Earth Day try a simple approach by benefitting our pollinators! Plant a Garden for Pollinators: A most rewarding effort for immediate gratification!

If you have a small yard or outdoor patio space, you can make a difference. Plant native perennials around your home to provide food for bees and other pollinators. Low on space? Place your favorite sun-loving perennials in large attractive planters next to the patio for all to enjoy. Bees, hummingbirds, and butterflies are forgiving and happy to share the space with you!

Ditch the water-guzzling annuals. Choose nectar and pollen-rich flowers with a range of shapes, colors, and bloom times. Seek out locally native plants as they have evolved regionally and are well adapted to the climate, soil, light, and water conditions. Many native bee species have co-evolved to feed exclusively on native flowers and need them to survive.

Na...

16

Have you decided to buy a new construction home? Having your own agent matters.

If you've been searching for your dream home for some time and have been challenged with low inventory, you're not alone.

Right now, the supply of homes for sale is still low. But there is a bright spot. Newly built homes make up a larger percentage of the total homes available for sale than normal. That's why, if you're craving more options, it makes sense to see if a newly built home is right for you.

But it's important to remember the process of working with a builder is different than buying from a homeowner. And, while builders typically have sales agents on-site, having your own agent helps make sure you have proper representation throughout your home-buying journey. As Realtor.com says:

7

Becoming A Home Maintenance Pro: Tips For New Homeowners

Buying a house is a big achievement and also the start of a long, rewarding journey. As a new homeowner, you have a lot on your plate getting familiar with your new dwelling, moving all of your possessions, and getting used to making mortgage payments. Home improvement will also become an important part of life moving forward, and it's wise to start on home maintenance tasks as soon as possible once you move in. Start your life as a new homeowner on the right foot with our guide to becoming a home maintenance pro.

- Start with a Deep Cleaning

Ideally, the home should be spotless when you move in, but it doesn't hurt to make sure every corner has been scrubbed. In addition to all the usual home improvement benefits of cleaning, scouring every corner of the house will help you spot any maintenance issues. Be sure to clean the areas around appliances, chec...

6

Creative Options for Your Homeownership Quest

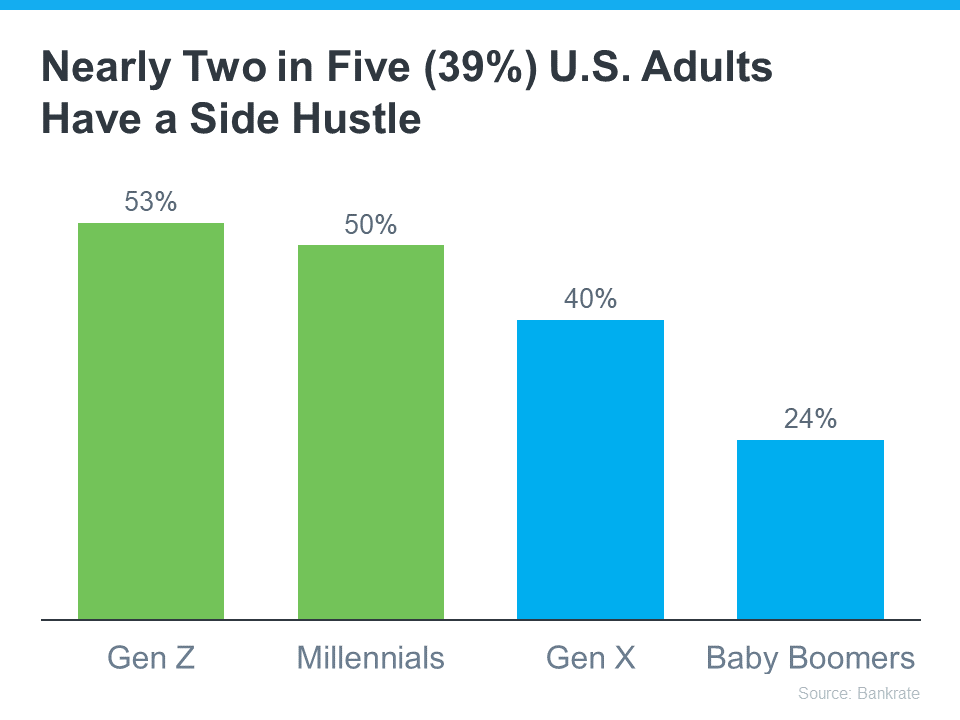

It may be time to consider creative options in your quest to become a homeowner. Think of a new home as a side hustle and not just in earned equity.

Does the rising cost of just about everything these days make your dream of owning your own home feel less within reach?? According to Bankrate, many people are seeking additional income through side hustles, possibly to cope with those increasing expenses and save for a home. This trend is particularly popular with younger individuals who may be dealing with student loan debt (see graph below):

14

5 Ways To Simplify Your House Hunt

Buying a house might be one of the most challenging purchases you make. It's an exercise in the physical, mental and emotional. For all the effort it takes from start to finish, the energy invested will pay off with an enjoyable and practical purchase to build wealth. These five tips will help you simplify the process.

1. Get your financial paperwork in order.

You will need to submit detailed financial records to the lender that may take some time to assemble. The sooner you start the process, the sooner the lender will be able to approve you for a loan.

2. Ask a mortgage lender to pre-approve you for a loan.

Pre-approval means that a lender is ready to finance a home purchase. By taking this step early, you'll know how much a lender is willing to loan yo...